Day One Biopharmaceuticals in the spotlight

Scientific deep-dive on data and investment potential

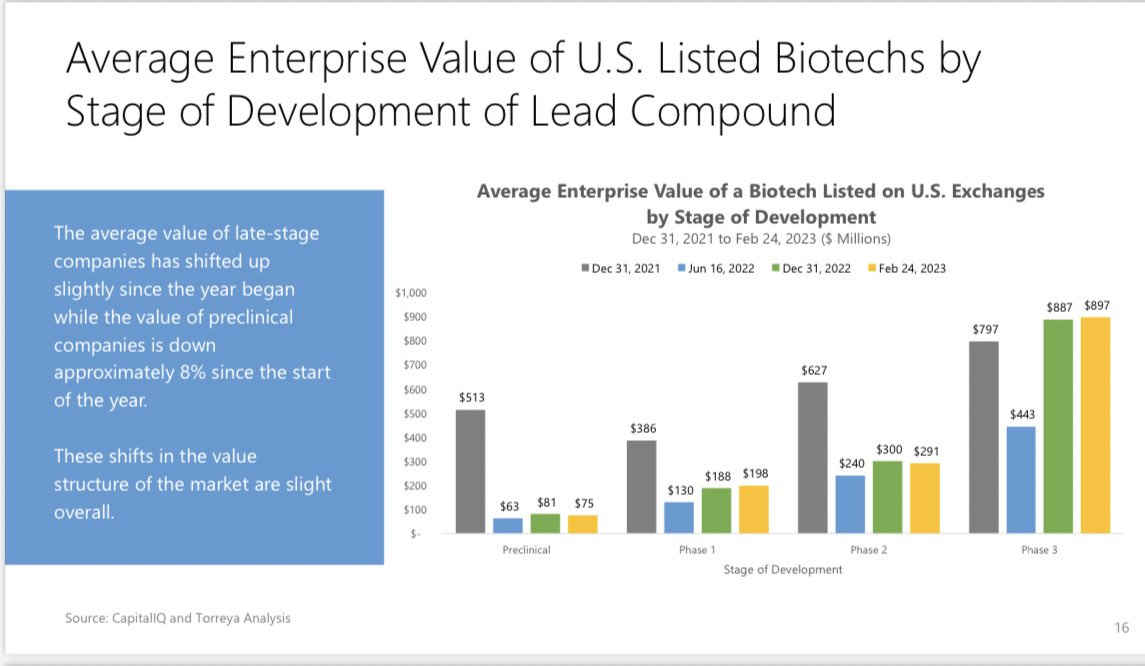

A report from Torreya determined that the average value of late-stage biotech companies has shifted up since December 2021, while earlier stage have seen values decline. Preclinical companies were hit hardest during this time, down an average of 85%, while Phase 1/2 names have fallen about 50%. Phase 3 companies have actually held up quite well, showing a strength in late stage and flight to safety.

Day One’s Drug Ready for NDA

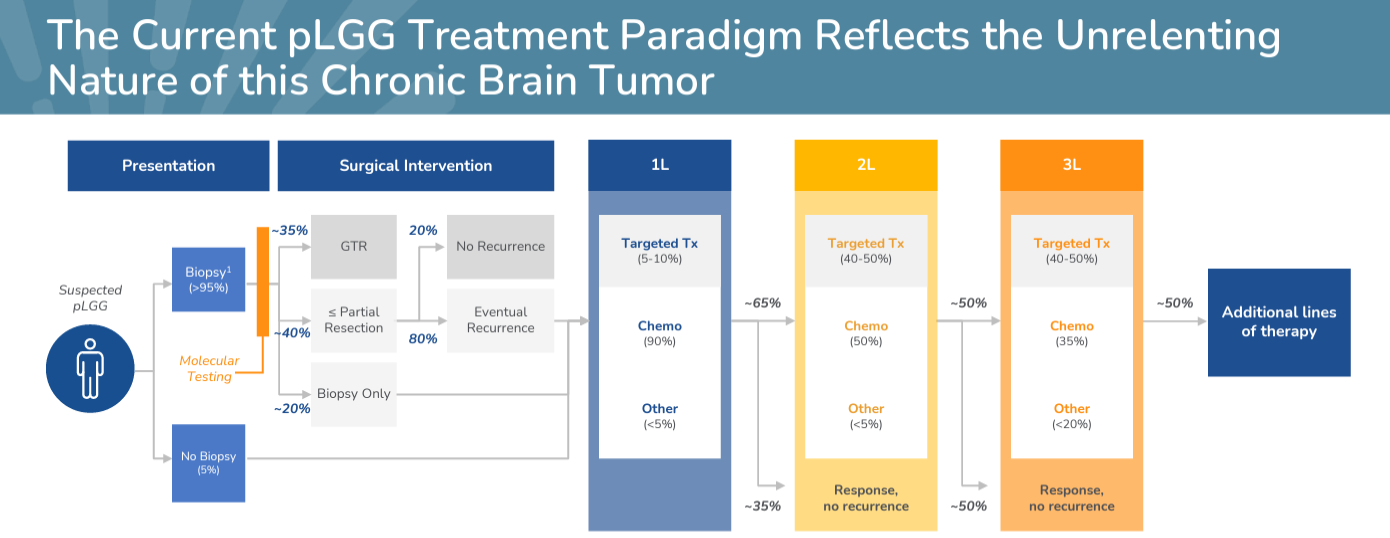

Day One Pharma ($DAWN) is developing tovorafenib (DAY101), an oral pan-RAF inhibitor for pediatric low-grade gliomas (pLGG). Despite being the most common brain tumor in children, there are no approved agents and no standard-of-care for the majority of patients with relapsed/progressive disease. Treatments include surgical interventions and chemo in early-line patients, with MAPK targeted therapy in relapsed/progressive cases.

Currently approved type I RAF inhibitors are indicated for use only in adults and patients 6+ years of age with relapsed tumors harboring a BRAF V600 mutation. These inhibitors can increase the risk of tumor growth in BRAF-fusion and other mutant cancers, which limits the risk/reward of the treatment.

DAWN’s target market is approximately 1,100 patients who have relapsed from prior treatment and have a BRAF-altered low grade glioma. For this orphan market, DAWN has reported promising pivotal Phase 2, with an NDA planned for mid-2023. The Company is also initiating a pivotal Phase 3 for frontline pLGG population, which should roughly double the patient population to more than 2,600 patients.

Data Update

In January, DAWN reported topline data on 69 evaluable patients.

44/69 (64%) patients reported a response. 34/44 responses were confirmed, and 10 responses were unconfirmed.

The median duration of treatment was 8.4 months, with 77% (n=59) of patients on treatment at the time of the data cutoff.

Safety based on 77 treated patients was generally well-tolerated with most common side-effects being change in hair color (75%), increased creatine phosphokinase (64%), anemia (46%), fatigue (42%) and maculopapular rash (42%).

Nearly 60% (n=46) of patients had already received at least one prior MAPK inhibitor prior to study participation.

Participants were heavily pre-treated, with a median of three prior lines of systemic therapy (range: 1-9).

Why Is This Important?

This data was important because DAWN was able to replicate much of the prior results in a larger sample size. Back in June 2022, DAWN announced initial data on the first 22 patients, in which 16/22 (64%) reported an ORR. This same response rate was replicated in the January 2023 update with 69 patients, as described above.

Additionally, in the first 22 patients, the spider plot showed that tumor change was flattening, showing a 75%+ change in tumor from baseline. 17 of 22 patients that were responders remained on therapy. The majority of patients were seeing significant tumor reductions. In other words, the drug seems effective in the first 22 patients.

This same chart was not shared for the n=69 data in January 2023. It will be an important update to see individual patient-specific data and update on treatment duration.

On the safety/tolerability front, DAWN will need to report similar profile in larger datasets to what was reported for the first n=25.

What Is Next?

DAWN will be providing an update on the data at a medical meeting in Q2 2023. It is important to keep an eye out for:

Update on the duration of response (DoR): latest DoR was 8.4 months. Needs to hit at least 12 months DoR.

Updating confirmed/unconfirmed responses.

Continued and well-tolerated safety profile. Low incidence of Grade 3 adverse events.

NDA submission for relapsed pLGG is expected for mid-2023. Additional Q2 data should provide a clear picture of what will be submitted to the FDA, including individual patient tumor data, DoR and confirmed responses.

With approximately 75M shares outstanding and a cash balance of ~$350M, DAWN trades at about a $1B EV. This is not a “cheap” price, given the Company’s initial indication is in relapsed pLGG, or about 1,100 patients. However, with a frontline pLGG study initiating in Q1 2023, belief is that existing data will be de-risking for a frontline setting that could double the incidence to 2,600 patients.

DAWN could present itself as a “flight to safety” name with potential movement as additional data is presented in Q2 2023.

Boutique Biotech has no position in DAWN.

P.S. Not investment advice. Read the Liability/Disclaimer subsection to learn more.